![]()

MIDDLE-MARKET HEALTHCARE

NET LEASE INVESTMENTS

Healthcare Net Lease specializes in the direct ownership, acquisition, and disposition of single-tenant net leased healthcare properties. We serve investors and medical professionals seeking income-producing real estate backed by essential healthcare tenants with long-term lease commitments and predictable cash flow.

The healthcare net lease sector stands apart from other commercial real estate asset classes. As CBRE noted in their 2025 U.S. Healthcare Real Estate Outlook, the medical outpatient building market is propelled by long-term demographic and healthcare spending trends that sustain a rising trajectory, distinguishing it from property types affected by short-term economic cycles. MOB occupancy reached a record 92.7% in Q4 2025 according to JLL, and MOB investment volume surged to $6.1 billion in Q4 2025 alone.

U.S. national health expenditures reached $5.3 trillion in 2024, or $15,474 per person, and accounted for 18% of Gross Domestic Product. CMS projects spending will reach $5.6 trillion in 2025 and continue growing at an average annual rate of 5.8% through 2033, outpacing GDP growth of 4.3% and pushing healthcare to 20.3% of GDP by 2033. This is not a cyclical trend. It is a structural economic force, and the real estate that houses these services is positioned for sustained, long-term demand.

100% Bonus Depreciation: Why Healthcare Properties Deliver Outsized Tax Benefits

The One Big Beautiful Bill Act, signed into law on July 4, 2025, permanently restored 100% bonus depreciation for qualifying property acquired and placed in service after January 19, 2025. Through a cost segregation study, investors can reclassify 20% to 40% of a healthcare property acquisition cost from the standard 39-year depreciation schedule into 5-year, 7-year, and 15-year asset categories that qualify for immediate 100% write-off.

Healthcare properties are uniquely rich for cost segregation due to the specialized infrastructure common across medical facilities. Qualifying components include medical gas piping systems for oxygen, nitrous oxide, vacuum, and compressed air; exam room cabinetry and millwork; specialized HVAC with HEPA filtration and negative pressure isolation; reinforced flooring for imaging equipment; lead-lined walls and doors for radiology suites; autoclave and sterilization systems; medical waste plumbing and disposal infrastructure; surgical suite lighting and high-amperage dedicated electrical panels for CT, MRI, and X-ray equipment; backup generator and UPS systems for life-safety compliance; water purification and reverse osmosis systems for dialysis; dental chair plumbing and compressed air lines; patient lift systems and ceiling-mounted tracks; nurse call and communication wiring; fire suppression systems designed for medical environments; data cabling and structured wiring for EHR systems; specimen pass-through cabinets; pharmacy clean room infrastructure; oxygen concentrator systems; and cryotherapy and cold storage systems. This density of depreciable infrastructure is why cost segregation studies on medical properties consistently identify a higher percentage of qualifying assets than virtually any other commercial property type.

Example: $5 Million Medical Office Acquisition. A cost segregation study identifies 30% to 40% as qualifying property, yielding $1.5 million to $2.0 million in Year 1 deductions. At a 37% marginal tax rate, that generates $555,000 to $740,000 in federal tax savings in the year of purchase. Compare that to straight-line depreciation over 39 years, which would yield approximately $128,000 per year. The investor receives four to six years of depreciation in Year 1.

For investors qualifying under Real Estate Professional Status (REPS), bonus depreciation losses from healthcare NNN properties can offset W-2 and other active income. Healthcare Net Lease coordinates third-party cost segregation studies as part of our acquisition advisory services for investors seeking to maximize first-year tax benefits.

WHY HEALTHCARE NET LEASES ARE PREFERRED BY TENANTS & INVESTORS

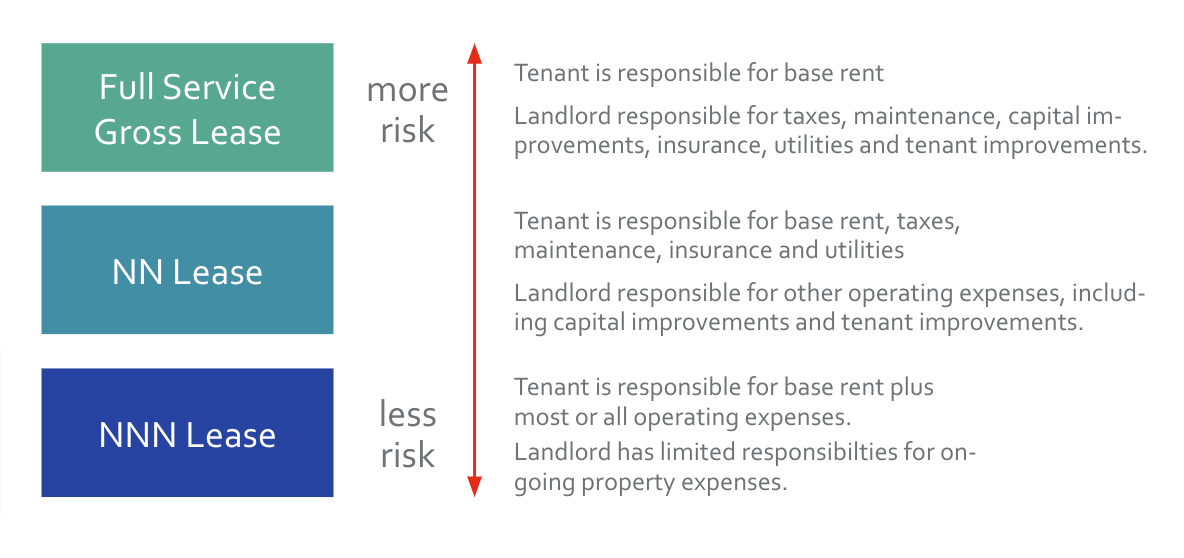

A triple net lease (NNN) requires the tenant to pay a base rent, plus most of the property expenses, including taxes, insurance, utilities, and capital improvements. This NNN structure helps the property owner avoid many unforeseen property maintenance expenses and, in turn, helps provide consistency in revenue.

Why Healthcare Tenants Are the Stickiest in Commercial Real Estate

Healthcare tenants sign long-term leases, typically 10 to 20 years with structured annual escalations now averaging 3% according to JLL, with average lease terms of 107 months. These are not variable or short-term leases. Many include renewal options that extend the income stream to 25 years or more.

Medical tenants invest $50 to $200+ per square foot in tenant improvements above the base build-out: MRI suites, surgical infrastructure, dental plumbing, dialysis water treatment, and specialized electrical systems. These investments make relocation economically prohibitive and drive renewal rates that consistently exceed other commercial property types.

The tenant base is also consolidating toward stronger credit. According to JLL, physicians in private practice declined to 42% in 2024, down from 60% in 2012. Health systems now account for 46% of MOB leases, bringing institutional-grade credit and balance sheets to the landlord relationship. This structural shift is strengthening the credit profile of the entire healthcare NNN asset class over time.

Net lease healthcare real estate properties are simple to understand, provide long-term predictable rental income, and are abundantly available across the country. Net Lease properties are typically stand-alone hard-assets with a single tenant. Very often healthcare businesses rent rather than build or buy their place of business, allowing them to focus on running their business rather than managing real estate.

Why Investors Prefer Healthcare NNN Properties

Healthcare NNN properties represent one of the most passive forms of commercial real estate ownership. The tenant pays base rent plus taxes, insurance, utilities, and maintenance, leaving the investor with predictable, net income and minimal management obligations.

Healthcare providers overwhelmingly prefer to lease their clinical space. Every dollar invested in clinical operations, equipment, staffing, and practice growth generates a higher return than a dollar locked in property ownership. This dynamic creates a natural and sustainable supply of healthcare NNN properties for investors, backed by tenants whose patient referral networks, equipment installations, and regulatory licensing are all tied to a specific address.

Properties range from $1 million single-tenant clinics to $20 million ambulatory surgery centers, offering entry points across the middle-market investment spectrum. Cap rates range from 5.00% to 6.00% for investment-grade health system tenants to 6.00% to 9.00%+ for non-investment-grade healthcare operators, providing options across the risk-return spectrum.

Healthcare Is the Largest Employer and Fastest-Growing Sector in the U.S. Economy

The U.S. healthcare industry employs over 22 million Americans in healthcare and social assistance, making it the largest employment sector in the country. Healthcare employment growth was 2.8% annually as of mid-2025 according to the Bureau of Labor Statistics, nearly triple the 0.9% growth rate for total nonfarm employment. No other sector in the U.S. economy is adding jobs at this pace.

National health expenditures grew 7.2% to $5.3 trillion in 2024, or $15,474 per person, and accounted for 18% of Gross Domestic Product according to CMS. Spending is projected to reach $5.6 trillion in 2025 and continue growing at an average annual rate of 5.8% through 2033, outpacing GDP growth of 4.3% and pushing healthcare to 20.3% of GDP by 2033.

A Growing and Aging Population Drives Structural, Non-Cyclical Demand

According to CBRE, the U.S. is undergoing a historic demographic shift in which the population aged 75 and older is growing by more than 1 million per year, triple the rate of the past 40 years. The 65+ cohort comprises just 17% of the U.S. population but accounts for 37% of its healthcare spending. Per capita healthcare spending averages approximately $8,000 for Americans under 65 but rises to over $20,000 for those 65 and older. The 85-and-older demographic is expected to nearly triple to 19 million by 2060, requiring the most intensive and facility-dependent care.

The Outpatient Migration Is Accelerating

According to Advisory Board data cited by JLL, outpatient volumes in the U.S. are expected to grow 10.6% over the next five years. Health systems led 53% of MOB construction starts in 2024, and MOB occupancy reached a record 92.7% in Q4 2025 according to JLL. CBRE reports that MOB construction completions will drop another 26% in 2026, reaching the lowest level in over a decade, while new construction rents are running at nearly twice in-place rents. This supply-demand imbalance is expected to push MOB rents to historic highs by the end of 2026.

Proven Durability Through Economic Stress

Healthcare NNN properties maintained occupancy through the Great Recession while traditional office vacancy spiked above 17%. Medical tenants cannot close their practices because of a credit crisis. Patients still need care. During COVID-19, healthcare facilities were classified as essential and remained operational. While retail and hospitality experienced 30% to 50% revenue declines, healthcare NNN rent collections remained above 95% for investment-grade tenants. Medical office has outperformed traditional office in occupancy, rent growth, and investor demand for 15 consecutive years. MOB availability sits at approximately 7% versus 18%+ for traditional office nationally. This is not an asset class that performs only in good times. It performs in all times, and that durability is what institutional capital, healthcare REITs, and private investors are paying a premium for.

Medical Technology and AI Are Expanding the Facility Footprint

Advances in diagnostic imaging, robotic surgery, genomic medicine, and AI-driven clinical tools are expanding the range of procedures that can be performed in outpatient settings. These technologies require specialized facility build-outs that anchor tenants to their locations and reinforce long-term lease commitments. The convergence of technology adoption and outpatient migration is accelerating demand for purpose-built healthcare real estate across every major metro and suburban market.

MEDICAL OFFICE

MEDICAL OFFICE

Medical office buildings (MOBs) remain one of the most sought-after asset classes in healthcare real estate. MOB occupancy reached a record 92.7% in Q4 2025 according to JLL, while average triple-net rents rose to $25.35 per square foot nationally. Rent growth has averaged 2.4% annually over the past three years, and JLL reports that new lease escalations now average 3% with average terms of 107 months.

The structural shift toward outpatient care has accelerated MOB demand through 2025 and into 2026. CBRE reports that MOB construction completions will drop 26% in 2026, reaching the lowest level in over a decade, creating a supply constraint that favors existing property owners. Health systems are relocating services out of hospital campuses and into community-based locations, and CBRE notes that only 19% of MOBs under construction are on hospital campuses, yet those account for 40% of the square footage being built.

Tenants range from large health systems with investment-grade credit ratings such as HCA Healthcare (S&P: BBB, Moody's: Baa3), Ascension (AA+), and Piedmont Healthcare (Aa3, upgraded by Moody's in 2025) to independent physician practices and specialty groups. Health systems now account for 46% of MOB leases according to JLL, bringing institutional-grade credit to the landlord relationship.

Cap rates for medical office properties in Q1 2026 range from 5.5% to 8.5% according to industry data, with investment-grade health system leases with 10+ years remaining trading in the 5.00% to 6.00% range and non-investment-grade medical office with shorter lease terms trading in the 6.50% to 8.00% range. JLL reports that national MOB cap rates compressed 60 basis points year-over-year in Q4 2025. Middle-market asking prices range from $1.5 million to $15 million.

AMBULATORY SURGERY CENTERS

AMBULATORY SURGERY CENTERS (ASCs)

Ambulatory surgery centers are among the fastest-growing segments of healthcare real estate. ASCs provide patients with the convenience of having surgeries and procedures performed safely outside the hospital setting, typically at 40% to 60% lower cost than hospital outpatient departments. The CMS 2026 Hospital Outpatient Prospective Payment System and ASC Payment System continues to provide incentives supporting ambulatory access, reinforcing the long-term viability of ASC investment according to JLL.

There are approximately 6,100 Medicare-certified ASCs operating across the United States. Nearly two-thirds are single-specialty centers, with gastroenterology, ophthalmology, orthopedics, and pain management leading in procedure volume. Multi-specialty ASCs are growing as health systems and physician groups consolidate surgical services. CBRE recently facilitated the sale of the HCA Surgery Center Portfolio, a two-property ASC and MOB portfolio in Texas and Utah, to Montecito Medical Real Estate.

For investors, ASCs represent a compelling NNN opportunity. Facilities require significant capital investment in specialized build-outs including surgical suites, recovery areas, sterilization infrastructure, medical gas systems, and high-amperage electrical, creating high switching costs that anchor tenants for the long term. Lease terms typically range from 10 to 20 years with annual escalations of 2% to 3%.

Cap rates for ASC properties vary based on operator credit, lease term, and partnership structure. Health-system-affiliated ASCs trade in the 5.25% to 6.50% range, while independently operated centers may command 6.50% to 8.00%. Asking prices typically range from $3 million to $20 million.

URGENT CARE AND SPECIALTY CARE

URGENT CARE AND SPECIALTY CARE

The urgent care sector has experienced rapid expansion, driven by consumer demand for convenient, walk-in access to medical services at lower cost than emergency departments. The U.S. urgent care market has grown to over 15,000 locations nationally, with both independent operators and health-system-affiliated brands competing for community market share.

Urgent care facilities are typically 2,500 to 5,000 square feet, purpose-built or converted retail spaces in high-traffic suburban locations. Major operators include Concentra (backed by Select Medical), CityMD (merged with Summit Health), and numerous regional platforms. Health systems including HCA, Ascension, and Advocate Health are aggressively building out branded urgent care networks to capture patient market share and serve as entry points to their broader referral networks.

JLL reports that psychiatry and behavioral health related service lines comprised 10% of healthcare leasing activity tracked in 2025, while specialty providers overall represented 36% of medical leases. This growth in behavioral health, physical therapy, and outpatient specialty services is creating new demand for purpose-built clinical space across suburban and community markets.

For NNN investors, urgent care and specialty care properties offer attractive yields due to the fragmented operator landscape and the predominance of non-investment-grade tenants. Cap rates typically range from 5.80% for health-system-backed locations with long lease terms to 7.50% or higher for independently operated facilities. Properties are generally priced between $1 million and $5 million, making them accessible entry points for middle-market investors.

DIALYSIS CENTERS

DIALYSIS CENTERS

Dialysis centers have emerged as one of the most liquid and institutional-quality asset classes within healthcare net lease. The sector is dominated by two operators: DaVita Kidney Care and Fresenius Medical Care, which together operate the majority of the approximately 8,000 dialysis facilities in the United States. U.S. Renal Care is a significant third operator.

Dialysis is a medically necessary, recurring treatment that patients require multiple times per week for the duration of their lives or until they receive a kidney transplant. This non-discretionary demand provides exceptional occupancy stability and revenue predictability for facility operators, which translates directly into reliable rent payments for property owners.

Both DaVita (S&P: BB+) and Fresenius (S&P: BBB, investment grade) maintain strong credit profiles. Leases are typically structured as absolute NNN with 10 to 15 year initial terms and annual escalations. The specialized build-out required for dialysis operations, including water treatment and reverse osmosis systems, medical waste infrastructure, and patient station configurations, creates significant switching costs that reinforce tenant retention.

Cap rates for dialysis centers reflect the strong credit profile and essential nature of the service. Fresenius-occupied properties with 11 to 15 years remaining on the lease trade at approximately 5.25% to 5.75%. DaVita properties trade in a similar range. Shorter lease terms and secondary locations push cap rates to 6.25% to 7.00%. Typical asking prices range from $2 million to $8 million.

Note: Senior care properties such as assisted living, memory care, and skilled nursing are generally operations-intensive and not fully triple net. These facilities depend heavily on operator performance, staffing, and reimbursement structures. Healthcare Net Lease focuses on the single-tenant NNN dialysis model and other fully net-leased healthcare asset types where the investor receives passive, predictable income without operational exposure.

MIDDLE-MARKET HEALTHCARE NET LEASE

BROKERAGE AND ADVISORY

Acquisitions, Dispositions, and Direct Ownership

Healthcare Net Lease provides middle-market brokerage and advisory services for investors and medical professionals seeking direct ownership of healthcare NNN properties. Our platform is specifically designed for buyers and sellers of single-tenant, income-producing healthcare real estate.

We source and underwrite properties across the full spectrum of healthcare asset types, including medical offices, ambulatory surgery centers, urgent care centers, dialysis clinics, dental offices, cardiology and radiology clinics, vascular clinics, and other specialty care facilities.

Services include:

- Sourcing of NNN healthcare properties for acquisition

- Cap rates of 5.00% to 6.00% for investment-grade tenants and 6.00% to 9.00%+ for non-investment-grade healthcare tenants

- Disposition advisory for owners seeking to sell healthcare NNN assets

- Due diligence review and analysis of title, appraisal, property condition, survey, and environmental

- Access to debt financing for healthcare property acquisitions

- Cost segregation and bonus depreciation strategy coordination with third-party specialists

Healthcare Net Lease brokerage, acquisition, and disposition services are exclusively provided by Investment Grade Income Property, LP, doing business as Investment Grade Healthcare, a licensed real estate brokerage. Healthcare Net Lease is co-sponsored by Investment Grade Healthcare and Responsible Real Estate Investment, LLC.

Healthcare Net Lease does not offer securities, legal, or tax advice. Investment and tax topics discussed are for educational purposes only and should not be considered professional investment, legal, or tax advice. It is recommended that you discuss your situation with your tax, legal, or financial advisor.